Quant tradingRThink like a traderTools of the trade

Data Analysis and Edge Extraction for Traders

Towards the end of last year, we ran a couple of free Zoom webinars on: Here are the recordings: Basics

Towards the end of last year, we ran a couple of free Zoom webinars on: Here are the recordings: Basics

dplyr 1.1.0 was a significant release that makes several common data operations more syntactically intuitive. The most significant changes relate

The changing face of market data providers Over the last few years, a number of new market data providers have

In Australia, if you’re serious about getting the job done effectively and efficiently, you might say: “I’m not here to

Imagine you’re a relatively small, independent trader trying to turn trading from a hobby into a serious business. If that’s

rsims is a new package for fast, quasi event-driven backtesting in R. You can find the source on GitHub, docs

rsims is a new package for fast, realistic (quasi event-driven) backtesting of trading strategies in R. Really?? Does the world

It’s easy to lose money trading if you do certain things: Trade too much (paying fees and market impact on

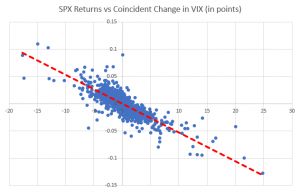

If you have some factor that you think predicts future stock returns (or similar) and you are making charts like

Many beginner traders don’t realize how variable the p&l of a high-performing trading strategy really is. Here’s an example… I

I’ve been helping a family friend with his trading. I’ve given him a simple systematic strategy to trade by hand.

Broadly, there are three types of systematic trading strategy that can “work.” In order of increasing turnover they are: Risk