R

How Much Damage Can I Do Turbo-Punting Shitcoins?

Here in Australia, we’re right in the depths of the silly season. We indulge in long lunches, take days off

Here in Australia, we’re right in the depths of the silly season. We indulge in long lunches, take days off

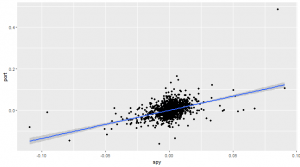

If you want to make money trading, you’re going to need a way to identify when an asset is likely

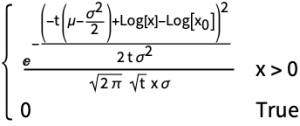

There are 2 good reasons to buy put options: because you think they are cheap because you want downside protection.

We’ve been working on visualisation tools to make option pricing models intuitive to the non-mathematician. Fundamental to such an exercise