R

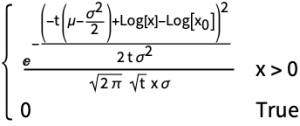

Probability Density Function for Prices from a GBM Process in R

We’ve been working on visualisation tools to make option pricing models intuitive to the non-mathematician. Fundamental to such an exercise

We’ve been working on visualisation tools to make option pricing models intuitive to the non-mathematician. Fundamental to such an exercise

This post summarises the key lessons of the academic literature that has been published on pairs trading. The key themes

One of the things I’ve noticed from staring at the screen all day for the last few months is that

In today’s post we are going to be extracting CoT (Commitment of Traders) reports from the CFTC website using a

In the eye of the recent storm, with VIX up over 50, many traders were looking to “short the VIX”

Optimisation tools have a knack for seducing systematic traders. And what’s not to love? Find me the unique set of

One of the keys to running a successful systematic trading business is a relentless focus on high return-on-investment activities. High

To say we’re living through extraordinary times would be an understatement. We saw the best part of 40% wiped off

What is Vector Autoregression The vector autoregression (VAR) framework is common in econometrics for modelling correlated variables with bi-directional relationships

Way back in November 2007, literally weeks after SPX put in its pre-GFC all-time high, Friedman, Hastie and Tibshirani published