- $123,000 in a year

- $759,000 in two years

- $4,685,000 in three years

- $29,000,000 in four years

- $179,000,000 in five years

OK, so what level of risk /return is realistic?

Have you ever heard of Renaissance’s Medallion Fund? Jim Simon’s work of quant trading art, the pinnacle of large scale systematic trading? What was the performance of the Renaissance’s Medallion Fund? If we believe this Bloomberg article then the long-run return characteristics from Medallion (after fees) was:- a mean return of 44%

- annualised volatility of 21%

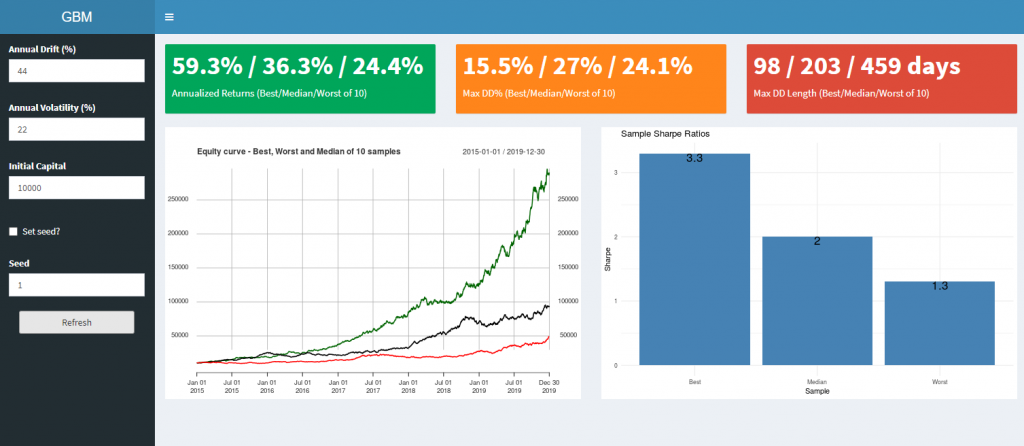

Here we have simulated 10 price paths with the long-run risk/return characteristics of the medallion fund (after fees).

We have plotted three of those price paths:

Here we have simulated 10 price paths with the long-run risk/return characteristics of the medallion fund (after fees).

We have plotted three of those price paths:

- The green one is the one with the highest returns – think of this as being very lucky with a very good edge.,

- The black one is the one with median returns – think of this as having an average amount of luck with a very good edge

- The red one is the one with the lowest returns – think of this as being very unlucky with a very good edge

What would investing in RenTech’s Medallion Fund Feel Like if we were Lucky?

Now, let’s concentrate on the highest performing of the 10 random portfolios. This is the green line. And its summary statistics are the first number in the green, orange and red boxes. If we were invested in the greatest systematic portfolio ever constructed (and could trade in the past before massively scalable cloud computing was available to everyone) and we were really really lucky, then we would have realised:- annualised returns of 59.3%

- a sharpe ratio of 3.3

In the greatest systematic portfolio ever made (the Rentech medallion fund), with a huge slice of luck, you still would have had to sit through a +15%, 6 month drawdown…What does this tell you about your ability to discriminate between whether something is good from a month or two of returns?

What Would Investing in Medallion Feel Like if we were Unlucky?

Now, let’s consider the red line… This is a return stream with the same characteristics as the Medallion’s historic performance – but this time we are simulating being unlucky.

In this case, we realised:

- annualised returns 24.4%

- a sharpe ratio of 1.3

In the greatest systematic portfolio ever made (the Rentech medallion fund), if you were unlucky, you would have had to sit through a 24%, 21-month drawdown…Do you think you can do better than RenTech – with their massive infrastructure, their phalanx of the smartest people in the world, their exchange rebates, their huge access to buying power, to dark flow, their scalability? Probably not, right? The only meaningful advantage you have is that you can go after very capital-constrained stuff that isn’t worth their time… (though my guess is that they are cost-efficient enough to go after quite a lot of that stuff anyway.)

What Does This Mean For The Trader?

You have to get rid of unrealistic expectations of a certain, steadily increasing equity curve. Market returns are noisy and uncertain. Even massive edges like Medallion’s need time to play out. You need to be realistic and patient. And you need to drop wishful thinking that there might be “something better”, a “trick nobody has realised yet”. There isn’t. It doesn’t exist. Market returns come with associated noise and market risk. The people on instagram and trading forums saying otherwise are lying liars and their pants are on fire. Appreciating and accepting this noise – this “mayhem” – is the key to trading enlightenment.- You will realise you will never and can never “figure out” the market.

- You will realise that simplicity and robustness are essential if you’re going to give yourself a chance.

- You will realise that good trading always “feels dumb” – because the short term results are utterly dominated by randomness.

- You will realise you don’t need to figure out the market. It appears we can identify bets with a reasonable chance of being positive expected value. We have to systematically throw a lot of those at the wall….and see what sticks.

Free Case Study:

A wantaway engineer’s journey into professional trading and out again

I went from engineering to an equity partnership at a prop trading firm to running my own systematic trading operation from home in Western Australia.

This case study is the full story – every mistake, every breakthrough, and some things I trade today.

Thank you for pointing out the reality. Just a 10 min search in Google shows many Get-Rich trading bots and methods. Expectations are high for beginners and reality is really different.

Given the above, i.e. 24% AR for the worse case scenario for best systematic portfolio ever made, wouldn’t it be reasonable to assume that the average retail trader with a decent level of knowledge, skills and experience couldn’t consistently make 1/2 of that on a good year? If that’s a reasonable assumption, why wouldn’t we simply invest in the S&P 500 index or top ten stocks, which have consistently made a 9.8% AR over the past 90 years?

I think that’s an entirely reasonable approach!! Nothing wrong with that at all.