OptionsQuant tradingR

Find Cheap Options for Effective Crash Protection Using Crash Regressions

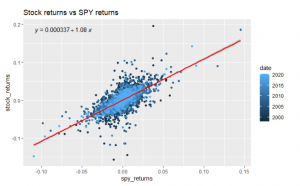

One way we can quantify a stock’s movement relative to the market index is by calculating its “beta” to the

One way we can quantify a stock’s movement relative to the market index is by calculating its “beta” to the

If you want to make money trading, you’re going to need a way to identify when an asset is likely

There are 2 good reasons to buy put options: because you think they are cheap because you want downside protection.