Quant trading

Much Ado About Variance

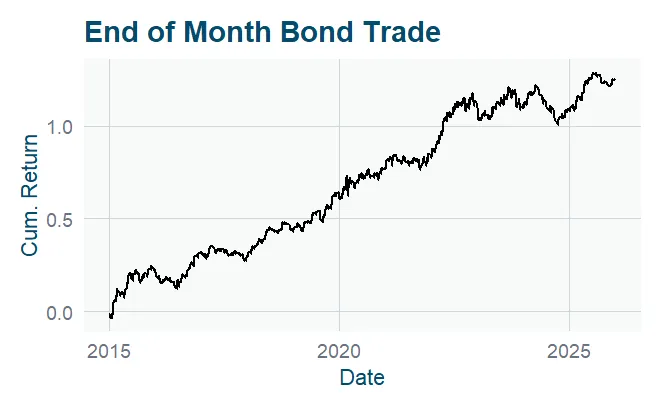

What’s Past is Prologue Let’s be honest: 2025 was a pretty good year to be a systematic trader. If you

What’s Past is Prologue Let’s be honest: 2025 was a pretty good year to be a systematic trader. If you

Traders love the illusion of precision. A few bad weeks go by, and you think, “Let’s run a t-test and

When I first got interested in trading, The Whitlams were all over Australian radio, and I was making all the

How do we find edges? First, we must be clear about what constitutes a good idea. It isn’t as simple

We’ve all used on/off type trading signals at some point. But you can nearly always extract more insight with a

Do you find yourself obsessing over p-values and t-stats when evaluating trading ideas? I get it. If you come from

The market is a highly competitive beast. If you’ve spotted an edge, others have too. And as capital piles in,

Recently, we had an excellent question on the Trade Like a Quant Discord server: “How do you know if your

The best trading edges are often found in places most people don’t think to look. It’s why being a bit

Someone sent me their trading technology blueprint. It was a thing of beauty: timeseries databases, Grafana dashboards, message queues, and

An easy, practical way to harness an edge in the face of trading costs is the “no trade region” technique.