Quant trading

Much Ado About Variance

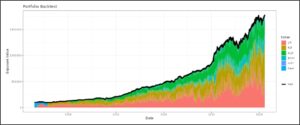

What’s Past is Prologue Let’s be honest: 2025 was a pretty good year to be a systematic trader. If you had a diversified portfolio of risk premia, you probably did alright. Claiming we did anything overly special in such a favourable environment would be a tad arrogant. That said, there’s a big difference between “the