RTools of the trade

How to Calculate Rolling Pairwise Correlations in the Tidyverse

How might we calculate rolling correlations between constituents of an ETF, given a dataframe of prices? For problems like this,

How might we calculate rolling correlations between constituents of an ETF, given a dataframe of prices? For problems like this,

Modern data science is fundamentally multi-lingual. At a minimum, most data scientists are comfortable working in R, Python and SQL;

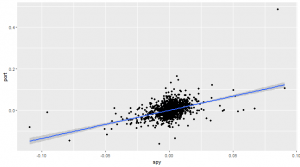

In this post, we’re going to show how a quant trader can manipulate stock price data using the dplyr R

Every aspiring millionaire who comes to the markets armed with some programming ability has implemented a systematic Get Rich Quick

In this post, we are going to construct snapshots of historic S&P 500 index constituents, from freely available data on

If you want to make money trading, you’re going to need a way to identify when an asset is likely

There are 2 good reasons to buy put options: because you think they are cheap because you want downside protection.

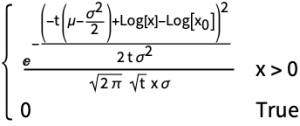

We’ve been working on visualisation tools to make option pricing models intuitive to the non-mathematician. Fundamental to such an exercise

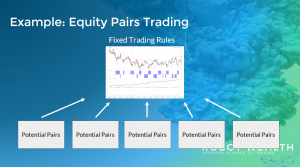

This post summarises the key lessons of the academic literature that has been published on pairs trading. The key themes

One of the things I’ve noticed from staring at the screen all day for the last few months is that

In today’s post we are going to be extracting CoT (Commitment of Traders) reports from the CFTC website using a

In the eye of the recent storm, with VIX up over 50, many traders were looking to “short the VIX”