What’s Past is Prologue

Let’s be honest: 2025 was a pretty good year to be a systematic trader.

If you had a diversified portfolio of risk premia, you probably did alright. Claiming we did anything overly special in such a favourable environment would be a tad arrogant.

That said, there’s a big difference between “the market was kind” and “I was prepared to capture what the market offered.”

So here’s a look back at what actually happened, what we learned, and one mistake I made that I really should have known better than to make.

The RW Team Evolved

We said farewell to James this year. He was always more a partner than an employee, and his contribution really helped lay the foundation for what Robot Wealth is today. He’s doing interesting work in the crypto space that’s very much worth watching, but he’ll always be part of the RW family.

With change comes opportunity. We welcomed Euan Sinclair to the team (if you don’t know Euan, he has a ton of systematic trading experience, particularly in options), and hired Ryan, a brilliant developer, from within our own community. Hiring from the community is such a bonus, honestly.

What Made Money

Here’s an uncomfortable truth that I’ll share anyway: you didn’t need to do anything overly special to make decent money this year. Diversified risk premia worked well across the board.

Stocks went up pretty much everywhere.

Bonds were a mixed bag. Long-dated treasuries were up just a tad, but exposure to the shorter end made money. Emerging market debt did well.

Commercial credit did alright.

And if you had gold in your risk premia portfolio, buy yourself a nice bottle of something special to celebrate. (Opinions are divided on whether it carries a risk premium, but there’s also a decent case for holding some as a diversifier.)

Volatility selling realised some of that famous negative skew during the April tariff tantrum, but was still profitable with even the most basic approach. Being a bit clever with the implementation (for example, selling the front of the VX futures curve and buying the back) was a good approach this year.

Systematic crypto edges continued to perform well, despite the big projects being down year on year. It feels like there are still good opportunities in crypto, but it did feel a bit harder this year. Maybe I’m just getting old.

Simple seasonality edges did well, such as end-of-month rebalance flow trades. Even simple convergence trades in equities worked really well.

I’m not going to pretend there was a lot of skill involved this year. A lot of it was just having fairly mundane exposures in place when the market decided to be generous.

But that’s the whole point of systematic trading: you don’t need to be a genius. You need to be positioned to capture what the market offers when it offers it.

Which brings me to the biggest lesson of 2025.

One Glaring Lesson

I really like simple seasonality edges. They’re easy to understand, easy to trade, and often surprisingly effective.

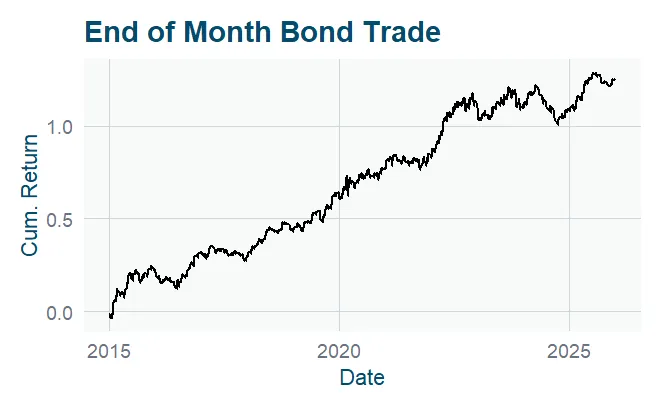

There’s a well-known calendar effect around turn-of-month flows in bonds.

Pension funds, insurance companies, and other institutional investors tend to rebalance at predictable times. And bonds may tend to be preferred towards the end of the month for “portfolio window dressing” reasons.

This creates temporary supply/demand imbalances that a patient systematic trader can exploit.

I’ve traded this effect for years. Buy bonds a few days before month-end, short at the close of the month, cover a few days after. Simple.

Historically, it’s been a Sharpe 1-ish strategy. Not spectacular, but solid. And importantly, it’s only in the market about half the time.

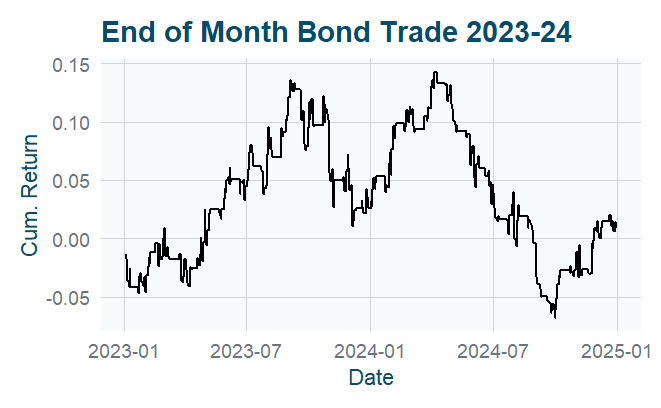

But starting around 2023, it had a rough stretch. The edge seemed to disappear.

So I did what any thoughtful, analytical trader would do…

I started telling myself stories.

Maybe market structure had changed. Maybe the participants driving the flow had shifted their behaviour. Maybe the trade had become too crowded.

All plausible explanations. All completely reasonable hypotheses.

And based on these stories, I stopped trading it.

Big mistake.

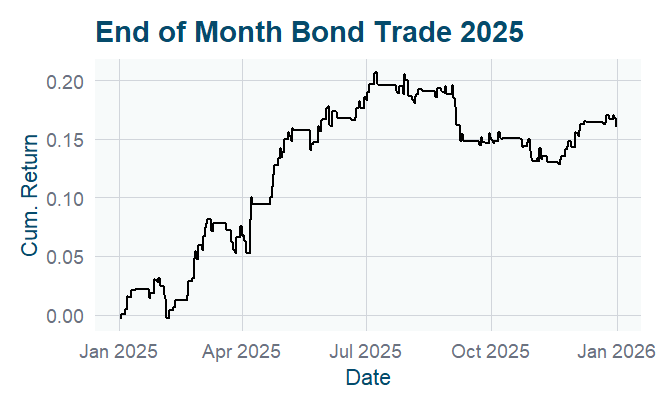

When I looked at the results for 2025, the turn-of-month bond trade would have returned about 15% at a Sharpe of 1.8 after costs.

That’s an excellent result for an insultingly simple strategy that’s only in the market half the time.

The Psychology of Abandoning a Sharpe 1 Strategy

Let me walk you through the maths of what I should have expected.

A Sharpe ratio of 1 means your expected annual return equals your annual volatility. If you’re targeting 10% returns, you should expect 10% volatility. That’s roughly a 16% chance of being down in any given year, assuming normal returns (which is generous).

So a Sharpe 1 strategy can easily be underwater for two years or more without anything being “broken.” That’s just what noise looks like at this Sharpe level.

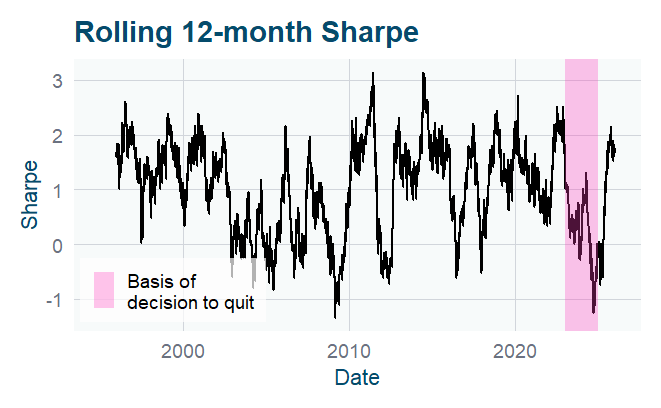

Here’s the rolling 12-month Sharpe of the strategy back to the mid-90s:

When I look at that rolling Sharpe chart now, 2023-2024 looks bad, but not unprecedented. It’s within the historical range of variation.

So why did I stop trading it?

I think it’s because the stories I told myself were plausible. If I’d had no explanation for the underperformance, I might have been more patient. But because I could construct a reasonable narrative about why the edge might have disappeared, I convinced myself that my judgment was adding value.

Turns out I was just pattern-matching on noise and calling it analysis.

The Stories We Tell Ourselves

This is the insidious thing about trading. We’re trained to look for explanations. Find the signal in the noise. Understand why things happen.

Trading as a job self-selects for naturally curious people who see detective work as an exciting challenge. We’re biased towards “figuring stuff out.”

But sometimes, there is no why. Sometimes it’s just variance.

The problem is that “it’s just variance” doesn’t feel satisfying. Our brains crave narrative. We want cause and effect. We want to understand.

So we invent explanations:

- “The market has changed”

- “Too many people are trading this now”

- “The underlying driver has weakened”

- “This only worked in a specific regime”

All of these might be true. Or they might just be stories we tell ourselves to justify abandoning something uncomfortable.

Unless the edge is based on a clear causal mechanism, I have no way to distinguish between “the edge has genuinely disappeared” and “this is just a bad run within normal expectations” in real-time. Neither do you. Neither does anyone.

This end-of-the-month bond trade is a classic example of something we have a plausible explanation for (noisy tendency of portfolio managers to window-dress holdings towards month-end), but no precise causal mechanism.

I don’t know who’s doing the buying and selling. I don’t know when they’re doing it. I don’t even know their true motivations. The reality is that this is a noisy effect resulting from a bunch of different people trading for different reasons, all happening at the margins amid the usual noise.

In that environment, you face a conundrum:

- Decent enough hypothesis for why it works on average

- Supported by data

- Sharpe ~1, so large variance in annual returns

- No observable mechanism to tell us when it stops working

The uncomfortable conclusion: you just can’t know if it’s stopped working from a year or two of lousy P&L.

But what I can do is set expectations in advance. Before I trade something, I should know:

- What’s the historical Sharpe ratio?

- How has it fluctuated in the past?

- How long might something like this be underwater?

- At what point would I genuinely conclude the edge is gone versus just experiencing normal noise?

And then I should stick to that plan, not revise it when the drawdown makes me uncomfortable.

The Discipline to Stick With Noisy Edges

I always urge people to have the right expectations about the edges they can trade as an indie trader.

Understand the underlying drivers of the edge. Be realistic about how much noise there will be in the short term. And be patient. Be disciplined. Turn up, run the process, don’t bullshit yourself.

If you’re really worried, turn it down a bit. Reduce position size. But don’t stop something you expect to go at Sharpe 1 completely just because it’s had a couple of rough years.

This is hard. I’ve been doing this for years, and I still got it wrong. The emotional reality of watching something bleed for 18 months is different from the intellectual understanding that it should bleed for 18 months sometimes.

But that’s precisely why systematic trading works. You’re supposed to follow the process even when it feels uncomfortable.

Especially when it feels uncomfortable.

Conclusion

2025 was a good year. But the lesson isn’t “we made money.”

The lesson is that having a systematic approach, a diversified portfolio of edges, and the discipline to stick with good but underperforming edges puts you in a position to capture what the market offers.

Some years, you get lucky. Some years you don’t. But over time, the process works.

You can only eat what you’re fed. But you have to be sitting at the table when dinner is served.

I’ll be sitting at the table for the bond turn-of-month trade in 2026. Lesson learned.

1 thought on “Much Ado About Variance”