Quant tradingRTools of the trade

How to Fill Gaps in Large Stock Data Universes Using tidyr and dplyr

When you’re working with large universes of stock data you’ll come across a lot of challenges: Stocks pay dividends and

When you’re working with large universes of stock data you’ll come across a lot of challenges: Stocks pay dividends and

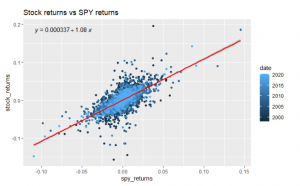

One way we can quantify a stock’s movement relative to the market index is by calculating its “beta” to the

Here’s a round-up of our new articles this week. They cover options trading, digital signal processing, data munging and Kris’s luxurious

Recently, we wrote about calculating mean rolling pairwise correlations between the constituent stocks of an ETF. The tidyverse tools dplyr

Working with modern APIs you will often have to wrangle with data in JSON format. This article presents some tools

In this post, we look at tools and functions from the field of digital signal processing. Can these tools be

How might we calculate rolling correlations between constituents of an ETF, given a dataframe of prices? For problems like this,

Modern data science is fundamentally multi-lingual. At a minimum, most data scientists are comfortable working in R, Python and SQL;

In this post, we’re going to show how a quant trader can manipulate stock price data using the dplyr R

Every aspiring millionaire who comes to the markets armed with some programming ability has implemented a systematic Get Rich Quick

In this post, we are going to construct snapshots of historic S&P 500 index constituents, from freely available data on

If you want to make money trading, you’re going to need a way to identify when an asset is likely